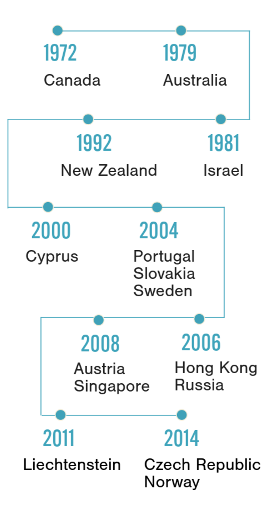

Over a dozen developed nations have abandoned the inheritance tax.

Inheritance tax is a tax imposed on the transfer of assets from one generation to another, typically following the death of an individual. While the exact mechanism may differ from country to country, the core principle remains the same: taxing wealth that is passed down, rather than earned.

It is viewed as a moral equaliser. Placing the tax burden on those inheriting significant wealth, often individuals who have done little to generate it themselves, the tax aims toredistribute economic resources more fairly across society. As the argument goes, those who inherit large estates can better contribute to the public good than those who rely solely on earned income.

Developed Countries that

Discontinued Inheritance Tax

Despite the moral and philosophical grounds, countries have increasingly turned their back on administering a tax on inheritance. This not only includes free-market havens but also social democracies like Sweden and Norway – countries that are long held as models of egalitarian governance.

What compelled these nations to bury a tax designed to address inequality?

– The tax did not align with a world where capital and those who own it move freely across borders.

– The tax was costly to enforce and didn’t make much economic sense.

– The tax unintentionally affected the families with modest wealth.

The tax did not align with a world where capital and those who own it move freely across borders

Studies have shown that even a small tax increase can lead to capital flight. Norway is a recent case in point, where a one percent increase in wealth tax has led to an exodus of many high-net-worth individuals.

Inheritance tax is no different. For instance, by the early 2000s, the inheritance tax had become economically self-defeating in Sweden. High net worth individuals like Ruben Rausing (Tetra Pak) and Ingvar Kamprad (IKEA) left Sweden, citing a punitive tax regime. With them, their businesses, investments, and philanthropic legacies crossed the borders. In 2004, Sweden abolished the tax, declaring the move to be important for improving the business environment of the country. This revitalised environment for succession planning and domestic entrepreneurship attracted entrepreneurs, including Ingvar Kamprad, back to the nation.

Hong Kong scrapped its estate duty in 2006. The logic was long-term competitiveness over short-term collection. As the mainland Chinese economy matured and talk of an estate tax grew louder in Beijing, Hong Kong positioned itself as a “safe harbour” for generational wealth.

Elsewhere in Asia, Singapore followed a similar path. It decided to repeal the estate duty in 2008 and leverage the move to send a strategic signal to the world – bring your wealth here, and we won’t tax your legacy. The goal was clear – attracting high net worth individuals would yield long-term, indirect dividends through capital inflows and high employment. The abandonment of the tax proved its worth as Singapore grew to become one of the most developed countries. It was reported that in 2023, its assets under management reached $5.4 trillion, with 78% sourced from foreign investors. There are over 2,000 single-family offices – private entities that manage the assets of ultra-wealthy families – in Singapore, and they are experiencing rapid annual growth.

Even Australia, which abolished estate and gift duties as early as 1979, has seen lasting reputational dividends. In 2023, it attracted over 4000 high-net-worth individuals. Its stable tax regime and absence of wealth transfer taxes remain a quiet but powerful magnet for private capital.

What these countries had in common was strategic realism: they understood that in a global marketplace of capital, tax policy is a branding decision and not just a fiscal tool.

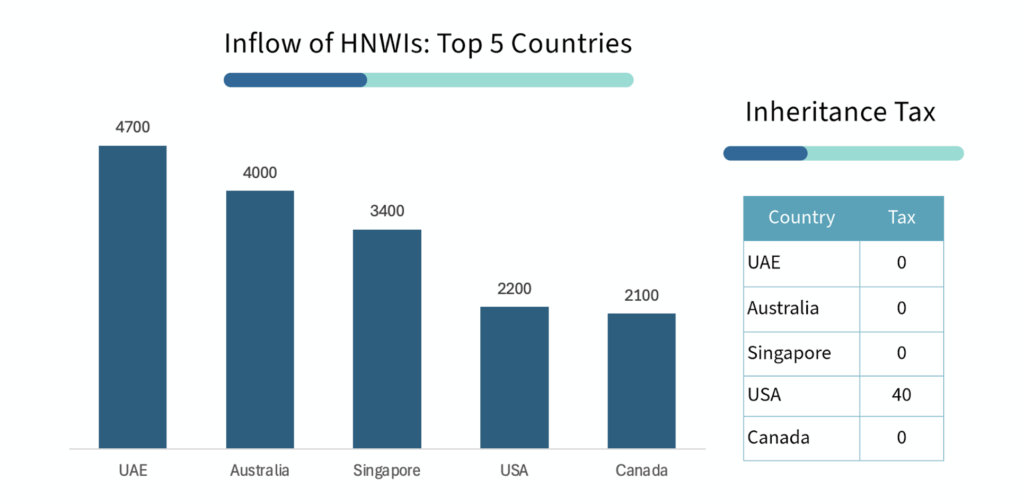

If we track the mobility of high-net-worth individuals (HNWIs) in 2023, a clear pattern emerges: countries attracting the largest inflows tend to impose no inheritance or estate tax.

Top 5 Countries with Highest Inflow of HNWIs

The United States might seem like an outlier, but its high exemption threshold of over $13 million means that the vast majority of people are unaffected by the tax. Currently, only around 0.08% of the adult death population files the tax. Despite retaining the estate tax, a Tax Foundation study has suggested that eliminating the estate tax could boost GDP by 0.08% annually over the next decade and generate an additional $8 billion in yearly federal revenue through increased economic activity.

The tax was costly to enforce and didn’t make much economic sense.

Inheritance tax has proven to be an inefficient, economically dubious, and administratively burdensome policy instrument. Even in countries committed to high public spending and universal welfare like Sweden and Norway, inheritance taxes have failed to deliver the kind of revenue that justifies their complexity.

In Sweden, inheritance and gift taxes never contributed significantly to the national budget. In 2004, it contributed to a mere 0.15% of GDP. The cost of compliance and the risk of capital flight far outweighed the relatively modest revenue of the inheritance tax.It eventually ceased to be a fiscally rational instrument.

Norway’sexperience echoed this. In 2013, out of the total taxable value of inheritance and gifts, the country could collect only 5% in revenue, which amounted to less than 20,000 Euros. The yield was so modest that the administrative and economic distortions it introduced were no longer defensible.

Illiquid holdings, inter-generational trusts, closely held businesses, and international asset diversification complicated the valuation of inherited assets. This was one of the reasons that many wealthy people engaged in tax avoidance schemes, spawning an economically unproductive planning industry. High-paid lawyers, accountants, and consultants spent countless hours engineering ways to reduce the taxable value of estates – resources that could be more meaningfully deployed in productive sectors. Enforcing compliance became a resource-intensive exercise. While the deadweight losses were hard to measure, countries realised that they exceeded any gains from tax. No wonder, New Zealand deemed estate and gift duties to be pointless before abolishing them in 1992.

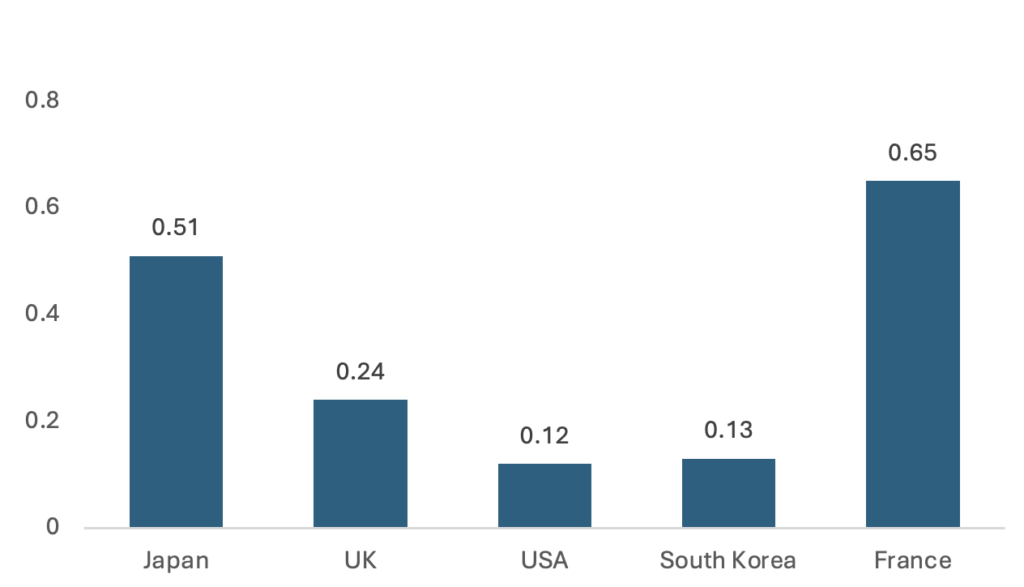

This is true even today – the revenue collected from inheritance tax in countries that continue to impose it is less than 0.7% of their respective GDP.

Percentage of inheritance tax to GDP (2023)

Inheritance tax was politically costly, too. In countries like Canada and Australia, its abolition was also driven by public choice dynamics. In both cases, governments faced a clear trade-off: retain an unpopular tax or preserve electoral support. They chose the latter.

The tax unintentionally affected the families with modest wealth.

Though often framed as a levy on the ultra-wealthy, inheritance tax has a long history of unintended consequences. Instead of redistributing wealth from the very rich, it has too often penalised families who are asset-rich but cash-poor.

A paradox: the truly wealthy can avoid it, while the merely well-off shoulder the burden.

In Sweden, before the tax was repealed in 2004, a growing number of cases emerged where surviving spouses or heirs were forced to sell family homes, summer cottages, or inherited farmland simply to cover the tax bill. These were not oligarchs or elites, but ordinary families in generational homes whose value had risen with the real estate market. The problem was particularly acute in a country where personal liquid savings is relatively low and there is high reliance on state welfare systems, leaving families without the cash reserves needed to pay large tax bills on inherited property.

This wasn’t just anecdotal. A 2004 government-commissioned report from Sweden’s Ministry of Finance noted that the inheritance tax was disproportionately burdensome on small businesses and family enterprises, as many heirs struggled to maintain operations while trying to meet tax obligations.

The United Kingdom also witnessed a similar tale, though it failed to do away with the tax. The ultra-wealthy often leveraged the Potentially Exempt Transfers, offshore trusts, and complex estate planning schemes to legally minimise their tax liability. By contrast, those with modest estates, often made up primarily of a single home or small business, were ill-equipped to engage in such planning. They were more likely to have assets locked up in property, more reliant on their full net worth for retirement, and less familiar with tax avoidance mechanisms. This made them easy targets for the taxman, even though they lacked the wealth that the tax was designed to capture.

A VALUABLE LESSON

This offers a valuable lesson for countries either considering implementing inheritance taxes or already burdened by them. Take the United Kingdom, for example: it enforces a 40% inheritance tax with a relatively low threshold of £325,000, pulling in many middle-income households. At a time when the UK is witnessing a significant exodus of HNWIs – 4,200 in 2023 alone – reassessing the inheritance tax regime could be a strategic move. This might not only improve capital retention but also enhance global competitiveness in the long run, improve political popularity, and save the merely well-off from the excess burden.